I’m a Trekkie. Once upon a time, I’d go so far as saying a hardcore TNG fan - give me five minutes of an episode and I could tell you the entire plot arc. So perhaps it’s not surprising that I ended up doing a stint in aerospace.

I remember walking in for my interview with the Chief Strategy Officer and seeing the walls lined with posters from all the communication satellites they had worked on (>80% of all the satellites that had ever been launched!), and thinking I’m sold… if this is the closest I can get to that final frontier, then I consider myself lucky!

Fast forward a decade, and here’s the serendipity of it all: I can’t get through the day without getting an inbound email asking for my expert opinion on satellite-to-device, or how Starlink is shifting the competitive landscape of telecom, or how much capacity AST SpaceMobile has to fulfill coming demand.

There’s a lot of glitter in the satellite space right now. Just look at AST’s meteoric stock rise from a <$3 stock price to $50 in about a year… and with how much revenue exactly?

As someone who’s been on the cutting edge of both telecom growth and aerospace, I thought it would be fun to create a lay person’s version of what needs to be true for satellite companies to succeed.

Disclaimer: This is the simplified, non-technical version. We’re not going down any rabbit holes about orbital mechanics or RF engineering - just some simple business fundamentals that matter.

The Three Critical Success Factors

For a company to operate satellite-to-device connectivity business at scale there are three key factors worth considering:

- Building the constellation

- Nailing the economics

- Driving demand

So let’s break each one down!

1. Building the Constellation

How to spend your billions of dollars in the coming years.

The bottom line? Getting to sustainable operations requires a LOT of time and A VERY LARGE amount of capital.

2. Economics: Choose Your Business Model, Accept Your Trade-offs

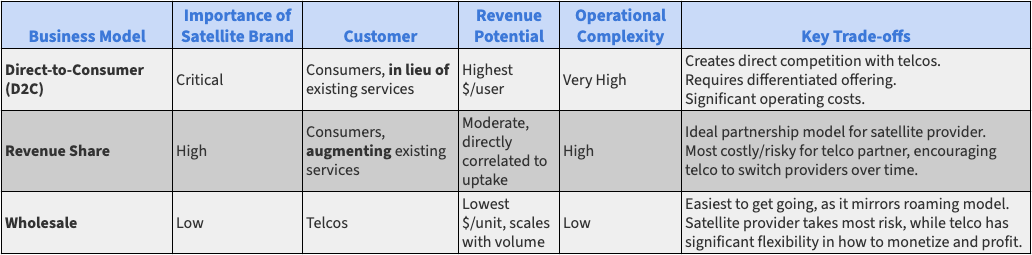

There are essentially three ways satellite providers can make money, each with different risk profiles and revenue potential:

- Direct-to-Consumer: Similar to the cell phone or home internet plan you have, the satellite provider can engage in a direct relationship with you. In doing so, you, the consumer, expect more than just the “technology”, but everything involved in an end-to-end customer journey experience.

- Revenue Share: Here the satellite provider steps back from their direct consumer engagement, but lends both their technology (and likely their brand equity too) for their go-to-market partner (i.e. a telco) to monetize the customer. The thesis for the satellite provider to have a share of the revenue stems from the fact that they are driving a significant portion of the incremental value the consumer is paying for - and often that value isn’t just in how the connectivity service functions, but actually in the selection of the service (via identification of the satellite connectivity brand).

- Wholesale: Typically targeted as a “cost plus” type of model, the satellite provider recognizes that they are, at their core, a capability provider (aka a vendor to their GTM partner), and prices competitively with the aim of driving volume of purchase and use.

While revenue share may be the sweet spot to target as a satellite provider, we have to remember that despite “unique” access to the satellites, it is the telcos that hold the leverage as the incumbent connectivity service - and from the telco perspective the wholesale model is much more beneficial.

3. Driving Demand: A Technologically Superior Product Without a User Base Is… Well… Betamax

Here’s where things get interesting. What experiences does satellite connectivity actually unlock, and how often will people use them?

At the end of the day, the longevity of the service that generally costs more than normal cellular service is going to rely on user behavior around both existing use cases, as well as those that have yet to be envisioned.

Let’s start with today, then, and heap on a healthy dose of honesty: if you live in the US, you probably have excellent coverage nearly everywhere you go! Maybe once a year you go camping in Yellowstone and don’t have service. Could satellite be the answer? Absolutely! But did you go camping to spend time doom-scrolling Instagram or texting your mom? Probably not.

The demand question breaks into several categories:

- Edge cases in developed markets: Camping, remote work, emergency situations. High willingness to pay, but infrequent usage.

- Rural broadband: Areas where the business case never worked for telcos to build infrastructure. High demand, smaller quantity, but strong willingness to pay.

- Developing markets: Countries where terrain made connectivity hard to deploy. Large potential market, but lower GDP impacts revenue per customer.

- Emerging applications: Use cases where satellite may approach cost parity with alternatives while providing unique capabilities (such as in IoT), or provide some unique capability that’s highly valuable when needed (such as burst usage of satellite connectivity during emergency disasters or times of network congestion).

The key insight: satellite connectivity isn’t about replacing terrestrial networks - it’s about filling the gaps where terrestrial doesn’t make economic sense.

Players to Watch

While SpaceX Starlink, and AST SpaceMobile may be consuming most of the oxygen right now (yes, that’s a bad space joke!), there’s a number of established and emerging players to consider:

- Amazon Kuiper: Long on the drawing and recently getting off the ground, Amazon both has the deep pockets, direct-to-consumer routes to market, and potentially unique access to launch slots

- Globalstar: An established player, providing satellite-to-device connectivity to Apple (also recipient of Apple investment)

- Iridium: A long time player in the GEO space, more heavily focused on IoT today

And more like Skylo, Lynk, Eutelsat OneWeb.

What Needs to Be True

If you were starting a satellite company or assessing one for investment, you’d want these key factors to be front of mind:

- Capital efficiency: reaching constellation deployment necessary to drive ongoing operations, without running out of money

- Regulatory alignment: access to appropriate spectrum and international coordination needed to operate

- Technology integration: ecosystem of targeted device manufacturers enabling their devices to connect directly to satellites

- Use case validation: demand emerging beyond the current state edge cases

- Economic sustainability: ability for the satellite provider to enact a revenue model that is sufficiently profitable, while acceptable by their partners

The Bottom Line

Satellite technology represents a genuine breakthrough in connecting the unconnected. The technology is finally mature, the economics are approaching viability, and the market timing feels right.

But as my aerospace background taught me: space is hard. Physics doesn’t care about your business plan, and economics don’t suspend themselves for cool technology.

I’m bullish on satellite connectivity - and on the use cases that are going to emerge as some of the current breed of satellite-to-device companies get hungry for revenue growth and creative about the use cases they explore.

Answering my titular question, I would say yes, space may well be the next frontier. But like any frontier, it’s going to be messy, expensive, and unpredictable. The winners will be those that shoot for the moon, but plan for the reality of outer space.